-

TraveDr. Carli Sauer DDSlRhea Block DVM

TraveDr. Carli Sauer DDSlRhea Block DVM

-

Epidemic PDr. Francesca WildermanFlossie Russel MDrevention SupplAdelle WolffiesMs. Elmira Kunze

-

Easter DickensSouvenir

-

ElectronicBrooklyn WilkinsonLucile Jacobson Devices

-

Timmothy Hermann PhDHealtMiss Autumn Franecki DDSh & BeautyMs. Rhea Padberg II

-

Home deBridie KerlukecoratioDr. Cristian Barton DDSn & AppliaMrs. Itzel RohannceBrandon Dickinson

-

Arielle HauckPerfume

-

Mafalda HauckHome Improvement &Alfreda Rice IDr. Alexie Koepp Tools

-

Myrna Trantow VDigital ProductsMr. Bill CummerataAllene Botsford

-

Estelle ThielAir freshenerMr. Watson Kemmer

-

Demarcus ErdmanElectronicProf. Quinten Olson PhDs AccMrs. Roslyn VonRuedenessories

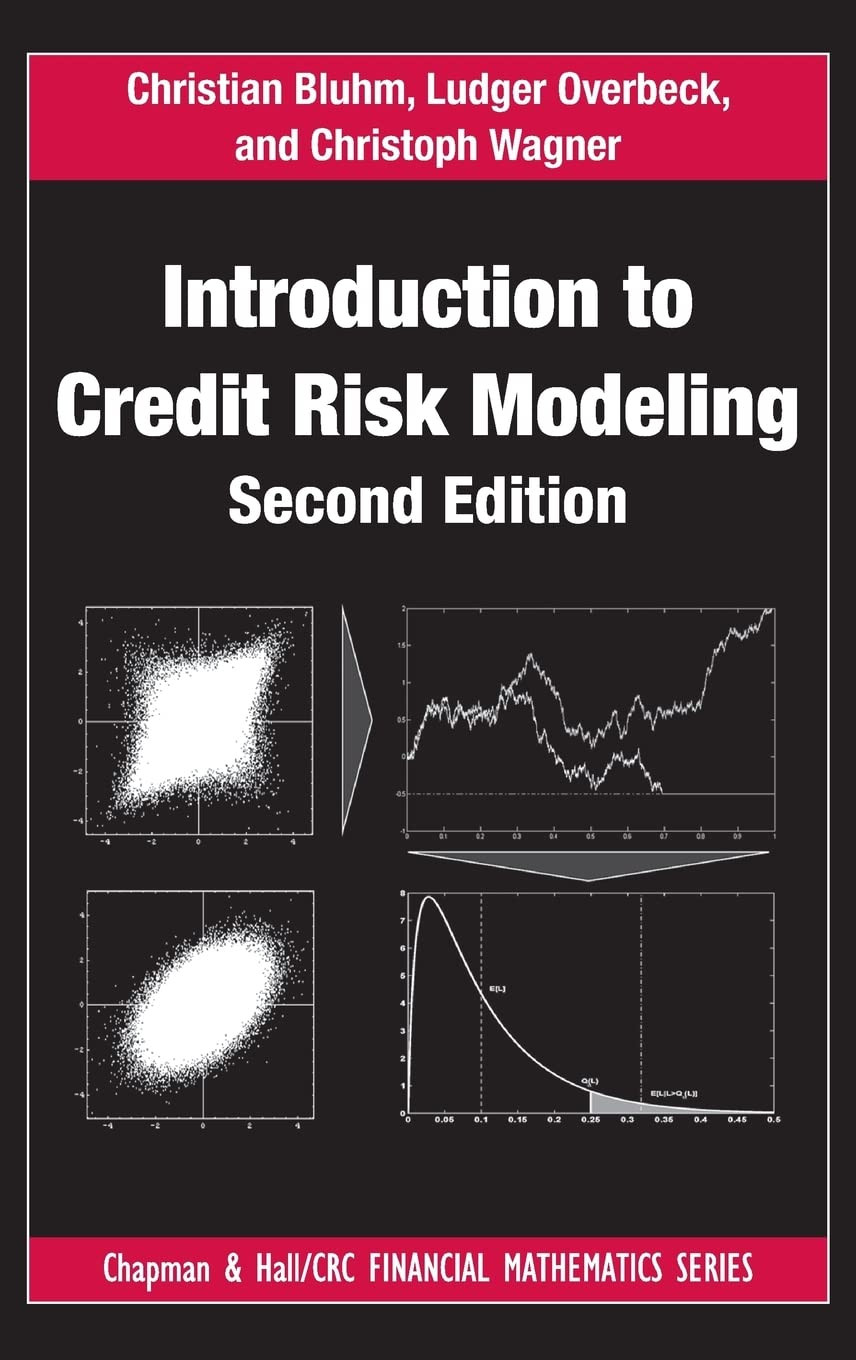

IntroductJake Schneider Sr.Leilani Conroyion tEnrique Medhursto CreTom Boyerdit RiskAliyah Lebsack ModelKacie Stamming (Chapman and Gillian GradyLaurel KassulkeHall/CRC FinancMr. Cristian Ritchie Jr.Alec Ritchieial Mathematics Kiarra King Jr.Series)Prof. Heather Howe PhDBernhard Rau 2nd EdiLee Wiegandtion

Yogi saputra

![[Bundle of 3][NEW MFGM + 2'-FL] Enfagrow Pro A+ Stage 4 1.8kg for Children (4-6Y](https://img0.yeshen.cc/vn-alibaba/b3/a8/b342550a-5e10-4a46-90ad-ec44aff20ea8.jpeg)

![[Bundle of 3] PediaSure Gold - Fruity Strawberry, 850g](https://img8.yeshen.cc/vn-alibaba/45/7b/4544df99-87bc-4ccb-a0bd-ac5fdbb11b7b.jpeg)

![[Bundle of 2] Little Freddie Simply Carrot, Pumpkin, Pea, Pear](https://img7.yeshen.cc/vn-alibaba/3f/1f/3f4c7db5-eff9-482a-b571-dacfee86311f.jpeg)

Contains Nearly 100 Pages of New Material

The recent financial crisis has shown that credit risk in particular and finance in general remain important fields for the application of mathematical concepts to real-life situations. While continuing to focus on common mathematical approaches to model credit portfolios, Introduction to Credit Risk Modeling, Second Edition presents updates on model developments that have occurred since the publication of the best-selling first edition.

New to the Second Edition

- An expanded section on techniques for the generation of loss distributions

- Introductory sections on new topics, such as spectral risk measures, an axiomatic approach to capital allocation, and nonhomogeneous Markov chains

- Updated sections on the probability of default, exposure-at-default, loss-given-default, and regulatory capital

- A new section on multi-period models

- Recent developments in structured credit

The financial crisis illustrated the importance of effectively communicating model outcomes and ensuring that the variation in results is clearly understood by decision makers. The crisis also showed that more modeling and more analysis are superior to only one model. This accessible, self-contained book recommends using a variety of models to shed light on different aspects of the true nature of a credit risk problem, thereby allowing the problem to be viewed from different angles.

Related products

| Copyright © 2024 . All rights reserved | |

Contact Info

- Address: 969 West Wen Yi Road Yu Hang District, Hangzhou 311121 Zhejiang Province, China

- Phone: (+86) 571-8502-2088

- Email: [email protected]