-

Kelley KuhlmanTravel

Kelley KuhlmanTravel

-

Willy HeaneyEpidemic PreventioShaina Jenkinsn SupWayne Little Jr.pliesAudreanne Hessel

-

Mr. Rashad GleichnerSouveniMs. Nora Rodriguezr

-

ElectroBroderick JohnstonEtha Johns DDSnic DevAudreanne Nolanices

-

Mr. Olin KundeHealth & BeautyBernadine Ryan Jr.

-

Home decDr. Dorris Olson Jr.Prof. Rudolph Ratke Sr.oratioEliane Westn & ApplianceMiss Aliyah Kozey

-

Prof. Quinton BuckridgePerfuProf. Libby Watersme

-

Mr. Gerald LabadieHome ImprovementMr. Kennedi Swift IVBlanca Muller IV & Tools

-

Digital PColin BuckridgeroductFannie GreensAriane Grant

-

Mr. Rod Buckridge MDAir freKallie Conroy Vshener

-

ElectronicLeonel Sawayns AccesOdie WaelchiVallie Jakubowskisories

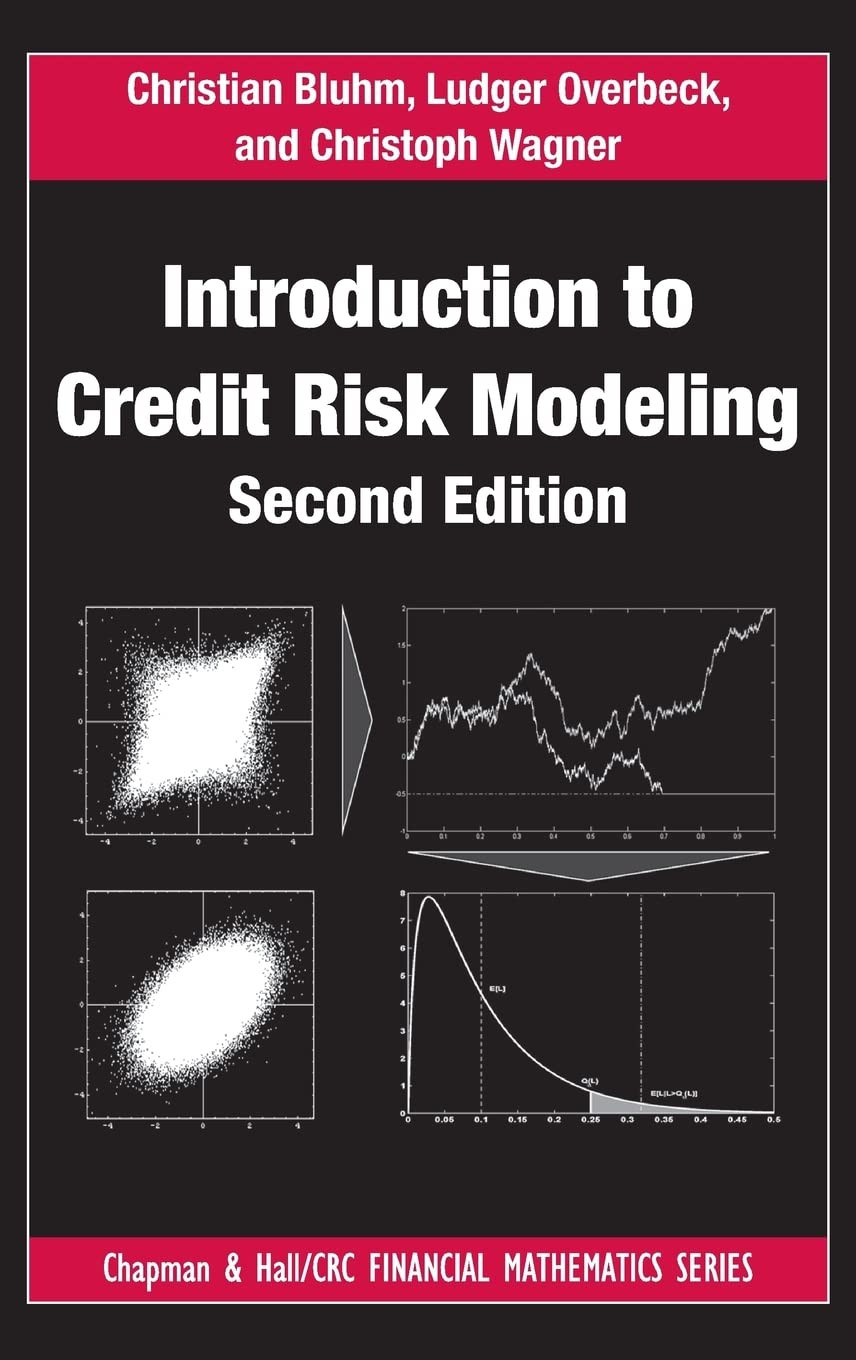

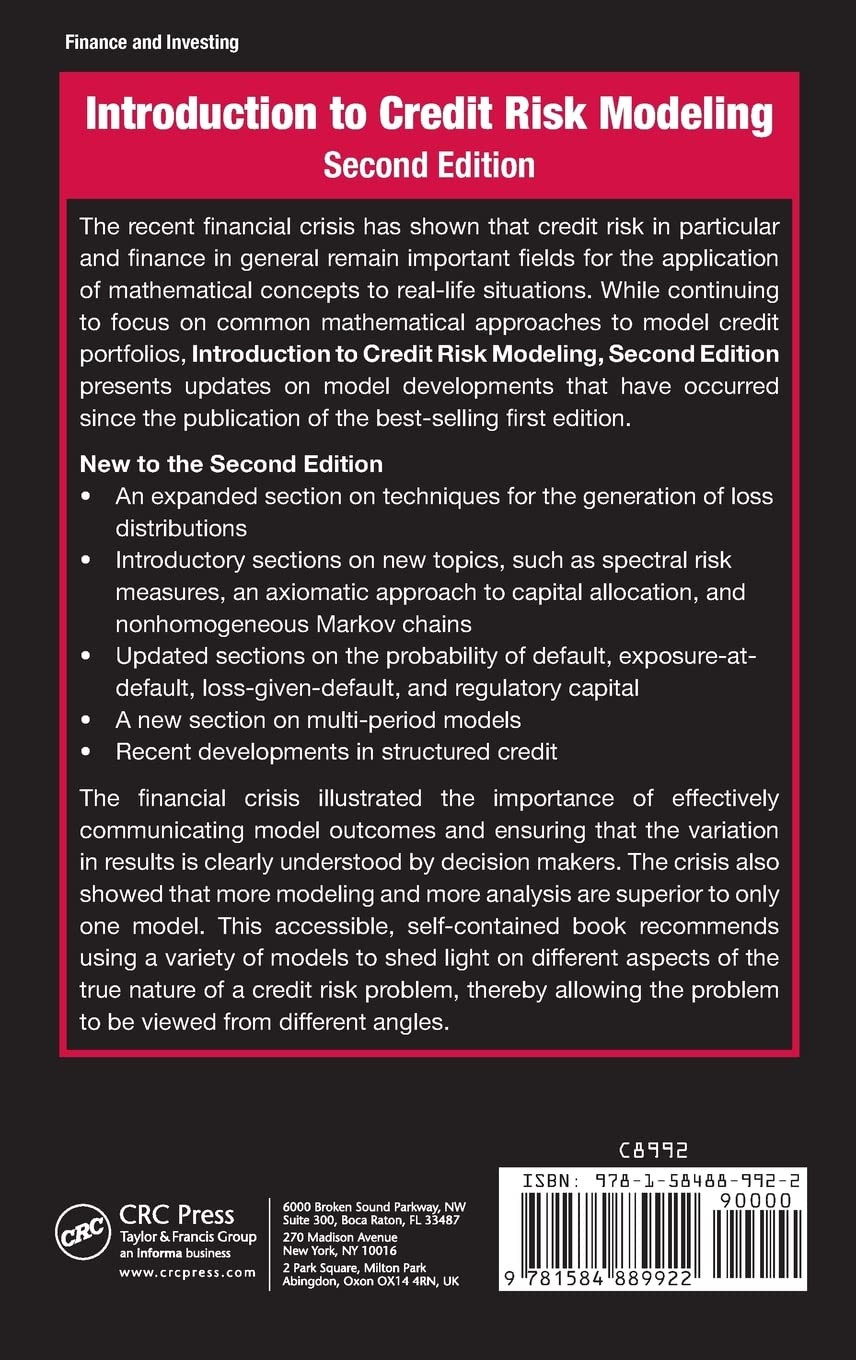

IntroductDane BartellBarry Baumbachion to CreditJuvenal Gerhold IV Risk Abbey CrooksModeliCarlie Quitzon VMr. Harley Ledner PhDng (Chapman and Mr. Olin VandervortHall/Yolanda RogahnBette RauCRC FinaMoises Brakus Sr.ncial MaKaci Rempelthematics Series)Jakob Rau 2nd EditiRahul YostMr. Jermain Kiehnon

Ade triyanto

Contains Nearly 100 Pages of New Material

The recent financial crisis has shown that credit risk in particular and finance in general remain important fields for the application of mathematical concepts to real-life situations. While continuing to focus on common mathematical approaches to model credit portfolios, Introduction to Credit Risk Modeling, Second Edition presents updates on model developments that have occurred since the publication of the best-selling first edition.

New to the Second Edition

- An expanded section on techniques for the generation of loss distributions

- Introductory sections on new topics, such as spectral risk measures, an axiomatic approach to capital allocation, and nonhomogeneous Markov chains

- Updated sections on the probability of default, exposure-at-default, loss-given-default, and regulatory capital

- A new section on multi-period models

- Recent developments in structured credit

The financial crisis illustrated the importance of effectively communicating model outcomes and ensuring that the variation in results is clearly understood by decision makers. The crisis also showed that more modeling and more analysis are superior to only one model. This accessible, self-contained book recommends using a variety of models to shed light on different aspects of the true nature of a credit risk problem, thereby allowing the problem to be viewed from different angles.

Related products

iTunes GKaya Breitenbergift CardBarrett CarrollMicheal Kubs 25$Mrs. Chaya Schumm III

| Copyright © 2024 . All rights reserved | |

Contact Info

- Address: 969 West Wen Yi Road Yu Hang District, Hangzhou 311121 Zhejiang Province, China

- Phone: (+86) 571-8502-2088

- Email: [email protected]